Here's the first 2 part of the series:

1. Retail bonds listed in SGX

2. Preference shares listed in SGX

First of all, about the terms bills and bonds. Bills refer to short debts (< 1 yr maturity )issued by the government while bonds are longer debts (>1 yr maturity). In my post, I'll treat all the debts issued by SG govt as bonds, to make it simpler.

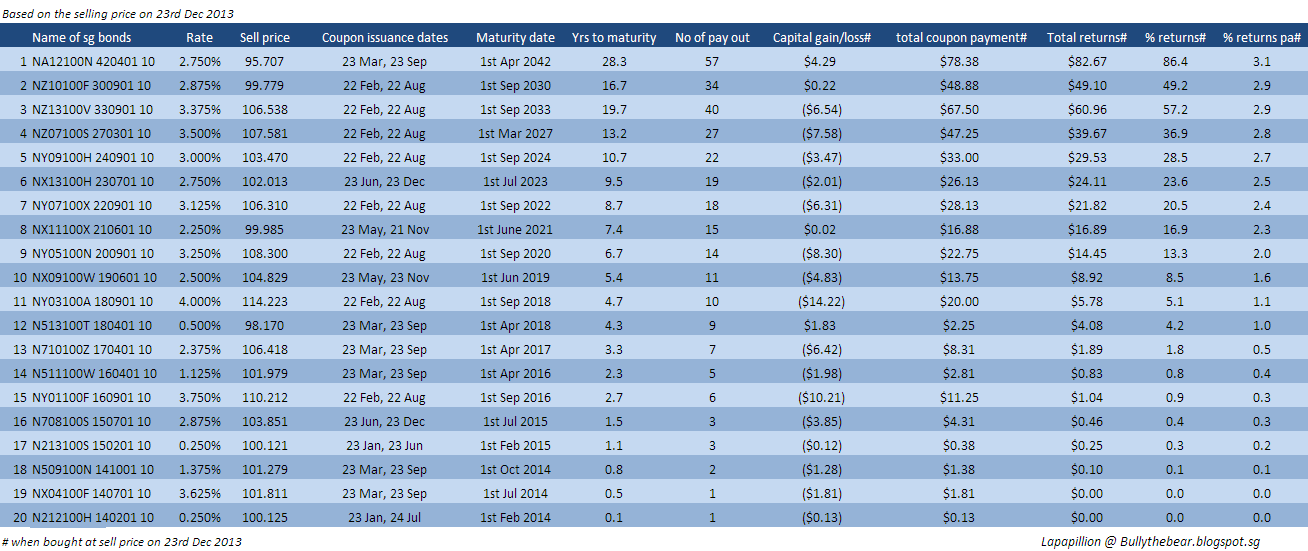

Here's the chart that I've compiled:

|

| Click to enlarge. I might be wrong, so do your due diligence. |

A few comments:

1. You'll notice that the yield are not fantastic, ranging from a coupon yield of anything between 0.25% to 4% pa. The yield, if you bought it at near current price, is worse off. Almost all the bonds are traded above par, so you'll get lower than the coupon yield listed on the name of the bond. This range from near 0% to 3.1% max. Usually for fixed income, the yield is inversely proportional to the perceived risk of the underlying issuing the debt. Since SG govt is quite unlikely to default, don't expect their yield to be like those in the Eurozone. You'll also notice that in general, the longer the maturity date, the higher the yield too. This is because the longer the period that you're holding the bond, you're exposed to more circumstances possibly leading to the bond being defaulted, hence you should be compensated for taking that greater risk.

2. We all know that in the near future with US stopping or reducing their printing, the interest rate environment would not be the same as it is now. It'll probably rise up, and that's a near certainty. Just how much and when. If you hold a bond till maturity, you don't have to worry about the rise of interest rate and the fall in price. Whatever yield you get is calculated at the extreme right of the chart above, because I've included the gains/loss due to the difference in par values and the market price of the bond. That being said, you'll notice that shorter maturity bonds are less sensitive to interest rate risk. So, if you're looking to put some money while waiting for the market to crash, for example, you might want to put into shorter term bonds. This way, you can still switch between asset class towards equity when the need and circumstance arises.

3. How safe are these instruments? If you treat fixed deposits as the ultimate safest, then sg bonds will rank right after it as the second safest. The difference in risk between the safest and the second safest is probably just a tiny gap, because even banks invest the money that you deposited with them in the fixed deposit accounts with Sg bonds, possibly along with other high grade bonds.

4. I would really like you to consider looking at those bonds between number 8 and 10. A typical fixed deposit with local financial institutions will be around 1.25% (possibly less) pa. If you lengthen your investment horizon to 5 yrs, you'll get around 1.6% pa by buying bond number 10. Increase a little more to 6.7 years, you'll get around 2% pa by buying bond number 9. I know it's nothing to shout about, but for those who have stashed aside a sum of money for wedding or for some major event happening in the near future (like within 6 years), then this is not such a bad place to park your money. With this short horizon, it's silly to put it into the stock market. You might lose the cost of a wedding banquet because you want to earn the interest to buy a rose!

This is not the only way to get sg bonds. The other way is to bid for it. I've never done it before, but I've seen such an option in internet banking. You can also get it through fundsupermart but there are fees involved.

0 comments :

Post a Comment